What Percent Of Income Should Go to Mortgage?

Taking on a mortgage is a big deal. It is an avenue through which you can buy your dream home, which is an excellent thing. However, if your mortgage is too high in comparison to your income, it can turn into a nightmare. You can find yourself in a load of debt with no end in sight. Even worse, you can end up losing the home of your dreams – and all of the money you have already paid into it. Like I said, nightmare.

The good thing is that it doesn’t have to be this way. With some knowledge, calculations, and strategy, you can take on the mortgage you need without breaking a sweat.

Rules Of Thumb

If you ask experts what percent of income should go to mortgage, they’ll typically go by a couple of different rules:

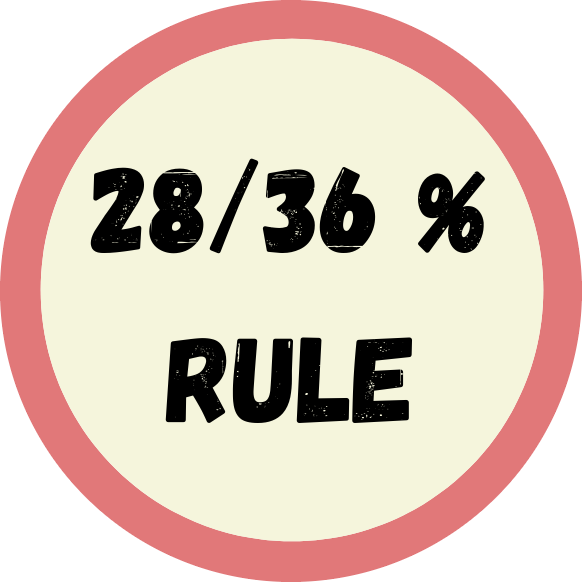

Rule #1: 28/36 Percent

This rule states that no more than 28 percent of your income before taxes should go to your mortgage payment, including interest, insurance, and taxes.

Additionally, it should not be more than 36 percent of your DTI or debt-to-income ratio.

Rule #2: 35/45 Percent

The 35/45 rule says that you should not spend more than 35 percent of your income before taxes on all of your monthly debt, which includes the mortgage payment.

This translates to 45 percent if you're calculating income after taxes.

Rule #3: 25 Percent

Some lenders use the 25 percent rule.

This simply states that your total monthly debt should not be more than 25 percent of income after taxes.

So which one should you go by?

The answer isn’t as simple as the question.

Different lenders use different rules when determining whether you can afford the loan, but here’s the rub: none of them are necessarily the best option for you.

Let’s be clear, these percentages can work – if you have no further obligations outside of your utilities and no other financial goals. However, they are simply rules of thumb – generalizations. They do not work for everyone.

No offense to any lenders. They are doing their jobs and following calculations that can work in a linear, perfect world. The trouble is that these calculations don’t take everything into account.

Debt-to-income ratios calculate things like:

Credit card payments

Personal loans

Auto loans

Child support

Student loans

These calculations don't consider things like:

Grocery money

Car insurance

School fees

Savings

Household necessities and so on

And because of that, you have to be your own mortgage specialist. What good is living in your dream home if you’re eating Ramen noodles every single night or can’t buy your kid a birthday present?

Before you dive into taking out a mortgage loan, it’s important that you figure out what percent of your income – not everyone else’s – should go to mortgage payments.

How To Determine What Percent Of Income Should Go To Mortgage?

We’re going to show you how to do this one step at a time.

Let’s start by gathering a few things:

Pen and paper

Calculator

Bank statements

Receipts for cash purchases

All current bills

This will take a little time and some concentration, so be prepared. However, you’ll be thankful you did this when you can comfortably pay for your mortgage.

Before we begin, I have to make something clear: this is not going to do you a bit of good if you’re not honest with yourself. If you spend $50 a week on coffee, this is not the time to try to hide it. No one has to see what you write down – this is strictly for your calculations.

Later, as you are working out your budget, you can use all of this information to decide where to cut back and how to prioritize expenses. For now, though, it’s time to make an honest assessment of your financial situation.

Okay, are you ready? Let’s do this.

Regular Bills and Ongoing Expenses

Start by making a list of all of your regular bills. We’re talking about things like:

Electric bill

Gas bill

Water bill

Car insurance

Gas for your car

Childcare expenses

Food

Internet

Charity

Pet care – if you have one

Gym membership

Phone payment

Cable, Netflix, or other streaming services

Amazon Prime

Pest control

Medication

Any amount you pay out every single month should be written down along with the amount. This includes lunch money for work, your daily coffee run, and even those candy bars you often forget about.

Now, it can sometimes be difficult to remember every little purchase, but that’s why you pulled out your receipts and bank statements. Taking a look at those will help you remember easily-forgotten purchases.

If you can take a little extra time, you might try tracking your expenses for two or three weeks. Just carry a notepad and pen around and write down every dime you spend. This will give you an even more thorough view of what you spend and where it goes.

Current Debt

Now it’s time to write out your regular debt payments.

How much do you pay on your credit cards each month?

Do you have any personal, auto, or student loans? Don’t forget to include any loans you’ve gotten from family or friends.

Irregular Expenses

These are those expenses that don’t occur every month but still come whether you like it or not. Some examples include:

Auto maintenance

Holidays

Birthdays

Doctor appointments

Taxes

Take some time to think this through. Anything that you pay throughout the year but that isn’t a regular, monthly expense needs to be added here.

Emergency Fund

Your emergency fund is an essential factor here. And if you don’t have one yet, you want to make sure that you do before you take out a loan.

You should have at least three to six months of expenses put away for a rainy day. And that amount should include whatever amount your mortgage payment will be.

Other expenses and spending

Now’s the time to consider anything and everything else.

If you go on vacation every year, add it in.

If you’re like me and your kids outgrow their clothes and shoes every other day, add it.

If you go to the movies or out to eat every Friday, add that, too.

Saving and investment

Hopefully, you are saving and investing regularly, and you want to keep doing that. Whether it’s $10 or $1,000 a month, write it down.

Time To Calculate

Now, it’s time to add all of those lovely numbers together. You can do this two ways, using whichever way works for you:

1st option

Multiply all of your monthly expenses by 12, and all other expenses by the number of times you pay them each year. You’ll then have an annual amount that you can subtract from your yearly income.

2nd option

Divide your annual and irregular expenses by 12 to get a monthly amount. Then, add that to your monthly expenses. Subtract that total from your monthly income.

How much do you have leftover?

That’s the amount you have left for a mortgage payment. If possible, you’ll want to use an amount a little smaller than that, so you have a cushion for unexpected expenses. Of course, it’s important to stick to your budget that you calculated, or you could easily fall behind.

What If I Don’t Have Enough For a Mortgage?

Don’t be surprised if this happens. Often, when you take a full assessment of your finances, you’ll find you have a lot less free than you thought. That’s not the end of it, though.

You can free up extra money by taking another look at what you pay out and finding ways to cut down.

Some questions you might ask yourself to do this include:

Do I really need to stop for coffee every day? Or could I invest in a good coffee pot and refillable mug?

Do I hit the gym often enough to justify that monthly expense, or could I work out at home for free?

Can we cut down on our weekly drive-thru visits to only once or twice a month?

Could I get cheaper auto or health insurance?

How many streaming services do we really need?

Go through every single line item and determine if there’s a way to cut it out or cut it down. Set a goal for yourself, something like cutting out $300 per month.

Think that’s impossible? It’s not. If you spend money on 30 different line items every month, you only need to find a way to cut $10 off of each item. It’s completely possible with some thought and determination.

Control Your Spending with Budgetry.

Conclusion

Remember, when it comes to loans and big purchases, you have to be your own financial specialist. You know your life better than anyone else ever could. So, if you want to take out a mortgage loan, it’s up to you to determine how much you can comfortably afford without sacrificing too many other things.

The good news is we have your back on this. With the Goalry mall, you have access to several financial stores that can help you do everything from building a budget to meeting your financial goals – like finding a mortgage loan. Sign up for your member key today and learn what it’s like to feel empowered and in control of your finances.